National Best

Modern Money SolutionParticipating Whole life insurance combines permanent life insurance with a tax-advantaged savings component and “Living Benefits”.

- Policy Cash Values grow inside your policy tax-free

- Guaranteed Cash Values that you can access during your lifetime

- Increasing Cash Values and Death Benefit that continually grow over time

- Take advantage of the Compound Interest Growth Curve with your money over time

- Tax-free Death Benefit and tax-free cash growth within your policy (According to today’s tax laws)

A major part of the reason that whole life insurance is such a great wealth building tool is the GUARANTEES that it provides.

GUARANTEED Level Premiums for Life

GUARANTEED Cash Values

GUARANTEED Never to Lose its Value

GUARANTEED Death Benefit

GUARANTEED Access to Your Cash Values

All of this as long as you pay your premiums. Option – 20 Pay or Life Pay

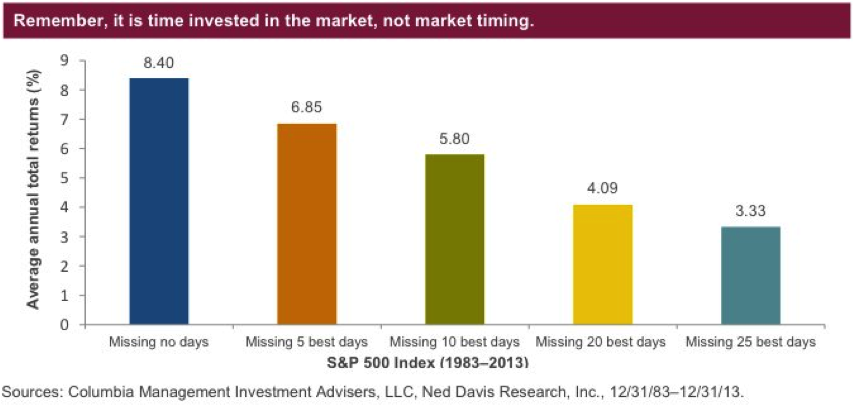

The key is time in the market, not timing the market.

When looking at the S&P 500 Index for the period 1983- 2013 (30 years equals about 11,000 days), o

If individual days can affect performance so dramatically, then why not be in the market for the good ones and out for the bad ones? Far easier said than done. Many investors try to time the market, chasing today’s hot investment or fleeing the latest downturn. Such a short-term perspective can harm performance and jeopardize your long-term financial goals. It is very difficult to anticipate the size and direction of the market for any single day. Just look at all the volatility in today’s market conditions and guessing the best day can be more like gambling which is not what you want to do with your hard-earned money. Patience and discipline is key to proper money management.

[2] Source: Heart and Stroke Foundation: 2014 Report on the Health of Canadians and 2017 Stroke Report.

- Starting at Age 20 : $1,027,696

- Starting at Age 30 : $593,010

- Starting at Age 40 : $326,150

- Starting at Age 50 : $162,322

In order to reach the same approximate $1 million goal by age 70, here is the approximate amount that would need to be invested each month to reach that goal with a consistent 5% return.

- Starting at Age 20 : $400/month

- Starting at Age 30 : $700/month

- Starting at Age 40 : $1,250/month

- Starting at Age 50 : $2,500/month

THE MORAL OF THE STORY IS TO GET STARTED AS SOON AS YOU CAN. IT IS NOT ABOUT HOW MUCH YOU CAN INVEST BUT IT IS ABOUT WHEN YOU CAN GET STARTED.

Well this may not sound like much at first glance, keep in mind that this is doubling EVERY 12 years. Learning to harness the power of compound interest for yourself and your family is one of the big secrets to achieving financial independence.

Using the same consistent 6% compounding rate of interest, we get the following returns:

- 2x your initial investment after 12 years

- 4x your initial investment after 24 years

- 8x your initial investment after 36 years

- 16x your initial investment after 48 years

- 32x your initial investment after 60 years

Put into real life scenarios, this means that a 22 year old putting aside $10,000 for retirement at age 70 would have $160,000. A 46 year old putting aside the same $10,000 would only have $40,000 at age 70.

The key is time in the market, not timing the market.

Guaranteed Investment Certificates (GICs) & Guaranteed Investment Accounts (GIAs)

Guaranteed Investment Certificates (GICs) offer fixed rates of interest for a specific term. Both principal and interest payments are guaranteed. GICs can be either redeemable or non-redeemable over the term. The Canada Deposit Insurance Corporation (CDIC) guarantees balances up to $100,000 for GICs with up to a

Guaranteed Investment Accounts (GIAs) have all the same benefits as the GIC as the principal and interest payments are guaranteed and offer a similar insurance coverage as the CDIC just through the insurance body known as Assuris.

PLUS ALL THESE BENEFITS that you can only get through your GIA from an insurance company …

Higher Interest Rates: Insurance companies rates are typically higher and more competitive than bank deposit rates.

Beneficiary Designation: A non-registered GIC account cannot have a beneficiary designation, but a non-registered GIA account can. This means the proceeds can go directly to a named beneficiary tax-free.

Estate Planning: At death, the proceeds from a GIC usually incur probate, legal and executor fees, not to mention the time it takes to settle the estate. GIA’s are an insurance product and do not have to pass through the estate. Your beneficiary may be paid directly and quickly, potentially avoiding estate-related fees.

Pension Income Tax Credit: GIC interest income does not qualify for the Pension Income Tax Credit, but interest earned on a GIA does. This means that an investor that is 65 or older may claim the first $2,000 of interest on a non-registered account as eligible pension income.

Creditor Protection: GIC’s, by themselves, cannot offer protection to the owner from his or her creditors. A GIA is an insurance product and, therefore, may provide creditor protection to the policy owner from his or her creditors

Annuity

The basic structure of an annuity involves the exchange of a lump of cash for the fixed income stream. A client who has worked his/her whole life and built up substantial savings will look to convert those savings into cash flow to help fund his/her retirement. This is the most common use of an annuity.

Annuities can be very flexible and have many variations but there are two basic structures:

Annuities can be very flexible and have many variations but there are two basic structures:

Life Annuity – ie. Cash flow for life

Term Certain Annuity – A stream of payments for a fixed amount of time. This can be particularly useful for creating cash flow to pay for a regular recurring payment for something over a fixed period.

Mutual Fund

Main Benefits include but are not limited to:

Professional Management • Diversification • Liquidity • Ability to invest a smaller amount

Segregated Fund

Maturity guarantees

Segregated fund policies provide guarantees of either 75% or 100% of the premiums paid (less a proportional amount of redemptions), depending on the product selected. These guarantees allow you to plan more effectively for life events such as your retirement.

Death benefit guarantees

Segregated fund policies provide a principal guarantee in the event of death. This death benefit guarantee is usually either 75% or 100% of the premiums paid (or policy value if you’ve locked in market gains with policy resets) less a proportional amount of redemptions, depending on the product selected.

Named beneficiary

You can choose one or more beneficiaries. These designations can be your estate, your children or other individuals, or associations such as charities.

Potential protection from creditors

Laws may protect a segregated fund policy in the event of bankruptcy or other action by creditors. It’s important to note that creditor protection may depend on court decisions concerning such laws, which can be subject to change and can vary for each province. This protection cannot be guaranteed.

Speedy estate settlement

Segregated fund policies can help speed up estate settlement with protection for you and your family. If you name a beneficiary, the death benefit isn’t subject to the delays and expenses of the probate process.

Lifetime income benefit option

Take control of your retirement and income by guaranteeing your income for life. With the lifetime income benefit option, your income won’t decrease regardless of how the segregated funds perform unless excess withdrawals are taken. You get protection against the risk of outliving your money, market volatility and inflation.

You can choose to receive guaranteed income for life on selected policies—speak to your advisor to learn more.

Guaranteed Minimum Withdrawal Benefits (GMWB) (Also known as a Lifetime Income Benefit Option)

GMWBs are built on a foundation of segregated funds where all or part of your investment is guaranteed after a 15-year period as well as on death. Additional guarantees are added so that you can withdraw a minimum amount of income every year for life, typically 5 percent of your investment starting at age 65. There’s the potential for growth as well as security with a GMWB.

Exempt Market Product Offerings

Why Invest in the Private Market?

The short answer is that research has shown the best investment strategies are ones that promote true diversification. Many are familiar with the success stories of the pension and endowment funds in Canada and the US. Private market products can comprise up to 40% of their total investment portfolio. That’s a large chunk and that is consistent across a number of successful pension funds. Canadian pension plans have among the highest performing investment portfolios in Canada. They diversify into non-market correlated assets by investing in private opportunities. These funds are well on their way to achieving the required rate of return for their beneficiaries.

The exempt market offers investment products that allow financial advisors to provide private investment opportunities to help properly diversify their portfolio like these successful funds do.

Portfolio Managers

Get In Touch

Head Office:

Unit#: 67B, 4511 Glenmore Trail SE,

Calgary, AB T3C 2R9

Phone: (403) 590-4500

Toll-Free: 1 800 503-6140

Fax: 1 877 904-7715